What is Financial Planning & Tracking?

Financial planning is the process by which an organization develops its budget, forecasting anticipated revenues and expenses using historical data and assumptions for future growth.

Financial tracking is the process of monitoring an organization’s income and spending over time, revisiting assumptions, and making adjustments as needed.

Why is it important?

- Financial planning and tracking helps organizations:

- Quantify their annual strategy and plan activities in a way that ensures feasibility and cost-effectiveness

- Align internal and external stakeholders around the costs and benefits of planned business activities

- Keep leaders informed on the health of the organization by knowing the gaps between projections vs. actuals

- Quickly identify any unanticipated expenses and course-correct appropriately

- Recognize when excess revenues allow for additional business or program investments

Best practices

Determine your budget team

- The financial leader of an organization typically leads the budgeting process; this may be the CFO in larger organizations or the Executive Director in smaller enterprises. Sometimes, a member of the board is involved as well. In many larger organizations, other senior leaders – such as the HR Director, Development Director and program / department managers – provide input and support as well.

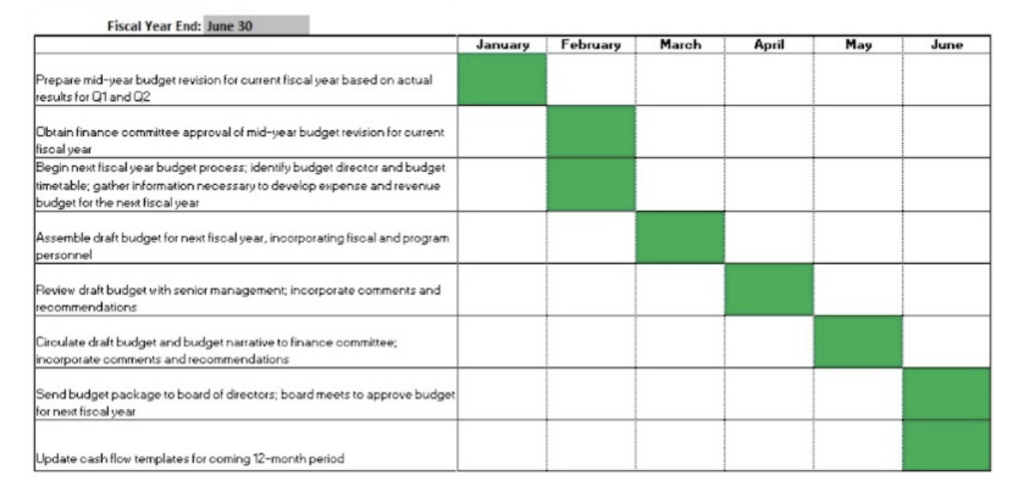

Develop a budget calendar to organize the process

- A budget calendar lays out the schedule of activities for developing a budget. It is helpful to establish a cadence for building each year’s budget.

- In the example below, the organization’s fiscal year ends June 30, and the budgeting process begins six months earlier. It is considered best practice for small-to-medium sized organizations to start the budgeting process three to six months before the end of the fiscal year. This allows enough time for assembling your team, gathering data, soliciting input, and presenting to your board.

- Here is a calendar tool you can use to monitor your budgeting process, as well as other fiscal management activities.

Gather information needed for the budgeting process

- Before diving into building a budget, pull together internal resources that will help guide and inform the new budget:

- Your strategic plan: The budget should reflect your strategic and financial goals for the year. This is particularly important if your organization anticipates significant changes in the upcoming year, such as expanding programming, launching a new business line, or starting a capital project.

- Your current budget: This gives insight into your organization’s thinking and expectations from a year ago and can serve as a guide.

- Last year’s income statement: Your previous year’s revenues and expenses can serve as a baseline to be adjusted based on expected changes for the upcoming year.

- Six-month and year-to-date results: Recent data on revenue and expenses highlight how close to or far from the current budget you have been.

- Current forecast for year-end: It is helpful to have a forecast for how you think you will end the year (Do you expect to hit your revenue goals? Will you go over budgeted expenses?). Having an idea of where you will land at the end of this year will make it easier to budget for next year.

- Multi-year forecasts: This projects your expected revenue, costs, and growth across a long horizon (3 or more years) and should be aligned with your long-term strategy (e.g., slow and steady growth vs. aggressive growth in launching a new business line).

Create the budget and plan for different scenarios

- To build your budget, you will need to project expenses and revenues for the upcoming year. To walk through an example nonprofit budget, explore this case study from the Nonprofit Finance Fund.

- Expenses are generally more within our control than revenue. Keep in mind the difference between variable costs (which change based on how much your business produces) and fixed costs (which stay constant regardless of production level) to identify potential savings. Also differentiate between direct costs (tied to a specific program or product) and indirect costs (organization-wide expenses that are shared).

- Expenses can be relatively straightforward to forecast if your main cost categories and levels remain similar to last year’s. However, if you expect significant changes in the year ahead (e.g., expanding to new cities, rolling out new products, or starting a big capital / building expense), you will need to factor in new / increased costs.

- Forecasting revenue can be more difficult due to the uncertainty of whether sales will come in at expected levels. It is risky to overestimate revenue, so try to base your projections on historical information rather than ideal outcomes. It can also be helpful to think about the likelihood of each of your potential revenue streams coming through and discount riskier revenue sources in your budget.

- Plan for a range of scenarios as you build your budget. Identify the scope of possible outcomes for revenues and expenses and think about what your best, moderate and worst case scenarios might be. Discuss these scenarios with your leadership team and create different versions of the budget that reflect these potential shifts.

- Here is a template for calculating different revenue scenarios.

- To make your budget flexible and easy to modify for different scenarios, incorporate adjustable operational variables. For example, build in “levers” for elements like price, quantity and discounts, so you can easily change them to see budget impacts.

- Once you and your leadership team have drafted a budget, solicit feedback from your finance committee and then present it to your board of directors for approval before the next fiscal year begins.

- Here are some tips for using your budget to communicate with your board and other stakeholders.

- After you secure board approval, be sure to debrief with your budget team and enter the approved budget into your accounting system.

Monitor actual performance against the budget on a regular basis, and course correct or reforecast as needed

- On a monthly basis, conduct a budget-to-actuals review, comparing your actual revenues and expenses to your budget. Investigate differences to understand why they occurred and determine whether you need to revisit your assumptions and/or adjust operations. Your budget is a management and operations tool that will help make sure you are heading in the right direction as planned.

- On a quarterly basis, update the board on your performance against budget, explaining variations and course corrections.

- If during the year your organization experiences a significant, unexpected change (e.g., the loss of a key funding source, major supply chain disruptions, or a change in regulations), you will want to reforecast your budget. This will mean creating a separate, revised budget that relies on year-to-date results as well as projections for the rest of the year.

Automate the budgeting process

- While spreadsheets are often used as an initial budgeting tool, over time it is more efficient to use accounting software to automatically generate frequently used reports (such as monthly budget-to-actuals) and send them to relevant staff. Once an accounting system is in place, make sure that actual expenses and revenues are recorded in the software using the same categorization as in the budget.

Acknowledgement: Resources from BDO Nonprofit & Grantmaker Advisory are represented in the content above.