What is Financial Reporting?

Financial reporting is the practice of summarizing the financial performance of an organization in standardized documents that include information on revenues / expenses (income statement), cash flows (statement of cash flows), and assets / liabilities (balance sheet). In addition, organizations can also report on metrics that are specific to their industry or business operations.

Why is it important?

- Financial reporting:

- Provides an organization with a consistent way of assessing its financial health

- Helps leaders make informed decisions (e.g., knowing which costs might be worth reducing)

- Gives external stakeholders, such as funders or investors, insight into the organization’s performance

- Eases compliance with government regulations and tax filing requirements

Best practices

Create accurate and timely financial statements on a quarterly and annual basis

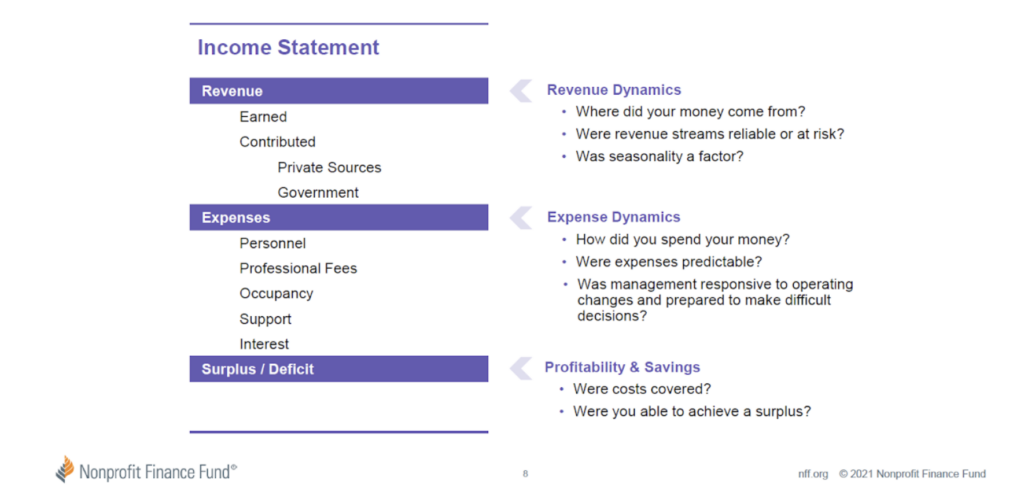

- Income statement (also known as profit and loss (P&L) statement or statement of activities)

- Shows your organization’s revenue and expenses over a specific period of time and the resulting profit or loss.

- For more on how to read and analyze an income statement, check out the Nonprofit Finance Fund’s webinar, slides and companion workbook on Financial Planning (Part 1).

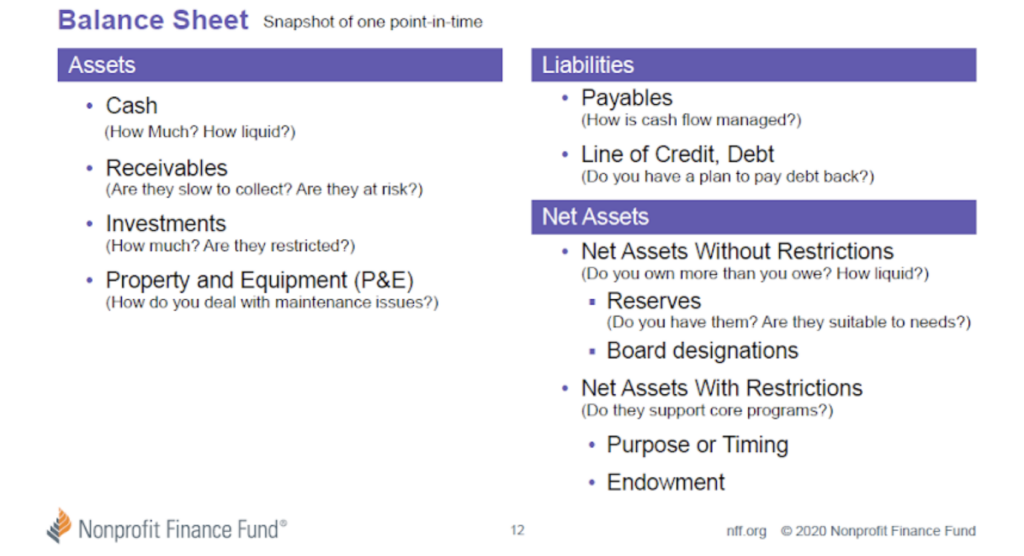

- Balance sheet (also known as statement of financial position)

- Shows your organization’s net worth at a specific point in time, listing its assets (what it owns), liabilities (what it owes) and resulting net assets.

- Review the Nonprofit Finance Fund’s webinar, slides and companion book on Financial Planning (part 2) to better understand the components of a balance sheet and what they say about an organization’s financial health.

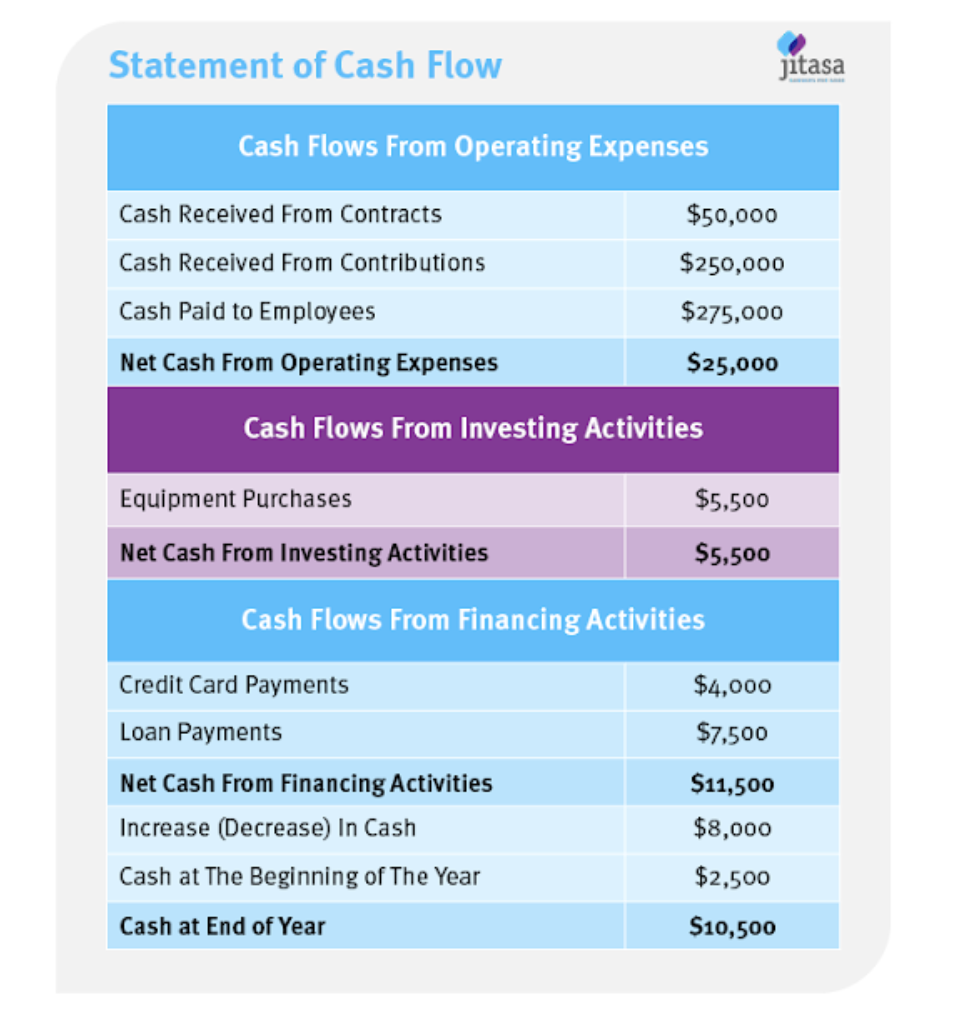

- Statement of cash flows

- Shows the movement of cash in and out of your organization over a specific period of time, giving insight into how much cash you have available to pay expenses.

- Learn more about the importance of cash flow statements and how to prepare one.

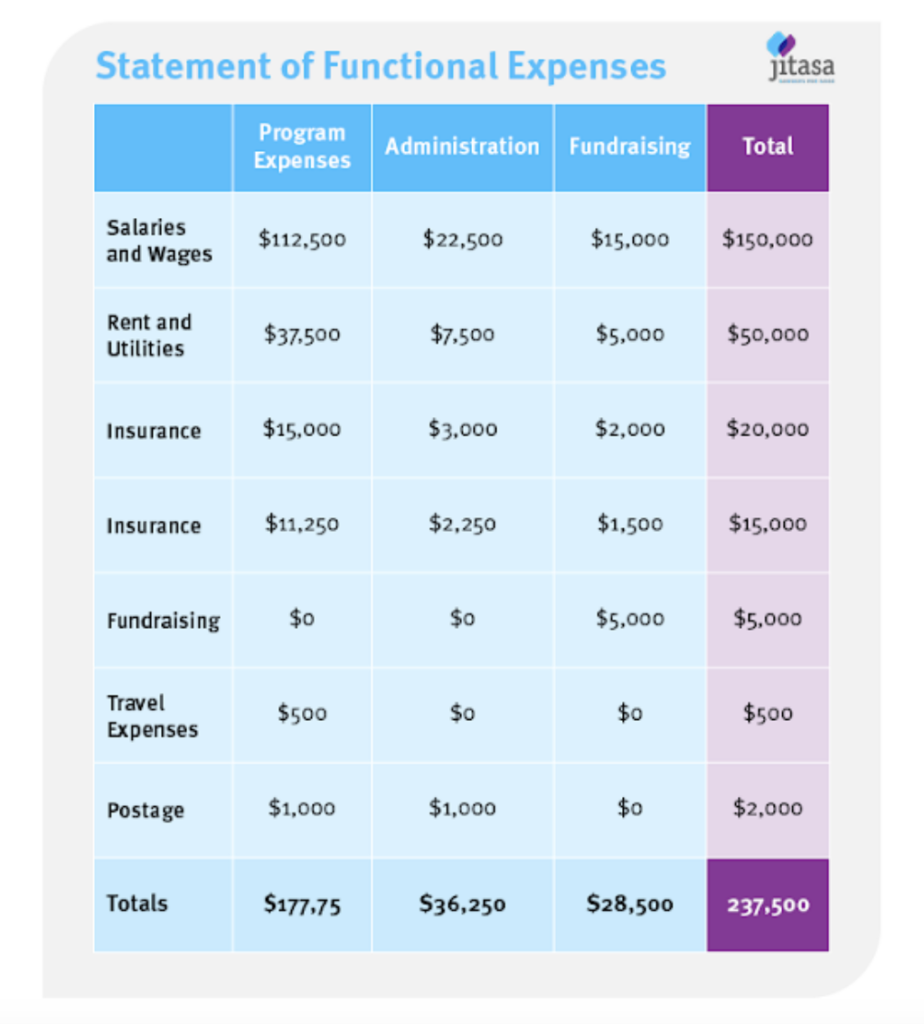

- For nonprofit organizations: Statement of functional expenses

- Shows how your organization spends funds, separating your expenses into three categories (program, administration and fundraising).

Regularly review commonly used financial reports

- If you use accounting software, it should be easy to generate income statements, balance sheets and cash flow statements for you to review regularly. These reports should be updated weekly to ensure that information is timely and actionable. Regular monitoring of reports will help identify financial trends and patterns, as well as spot potential issues early on.

Create additional reports that could help guide your business operations

- Develop additional reports that answer commonly asked financial or operational questions about your business. For example, if you invoice customers for services, it may be helpful to create an AR aging report (accounts receivable aging report) to identify which customers are paying on time and which ones are months behind – so you can follow up to improve your cash flow and reduce the risk of bad debt.

Analyze and discuss data from your financial reports to inform strategy

- Regularly discuss finances during your leadership meetings to make sure your team is up to date on the organization’s financial position. Proactively monitor key financial health indicators so you can make informed decisions about your operations and strategy. For example, if you notice fluctuating revenue in your income statements, you might consider taking on more debt to stabilize cash flow.

- Here are some common financial indicators that are useful to monitor:

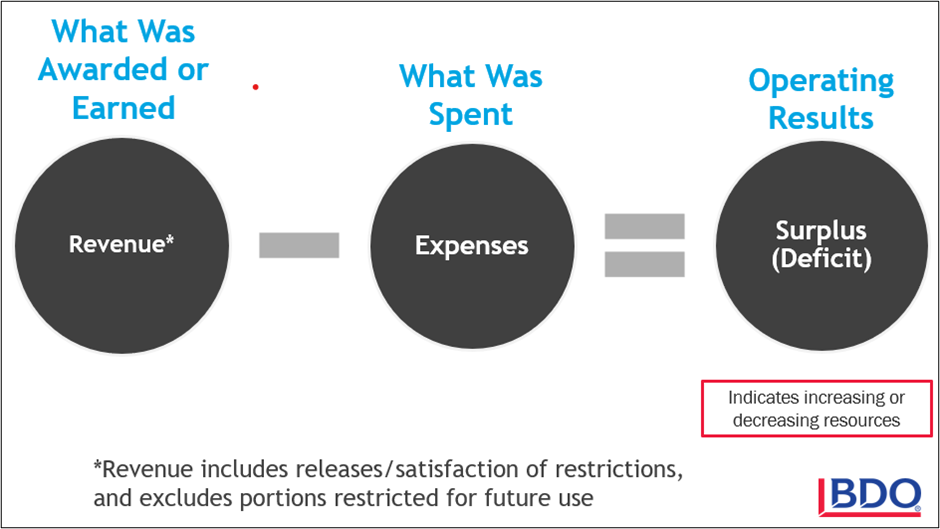

- Operating results: Analyze the income statement to understand if your organization is generating a surplus.

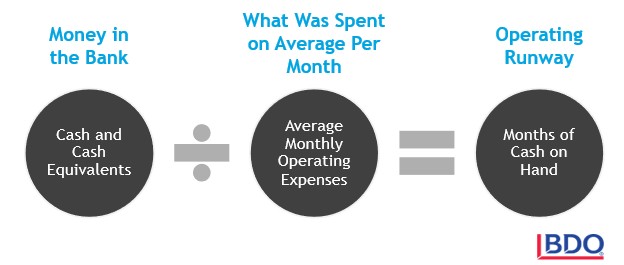

- Liquidity (months of cash on hand): Look at the balance sheet to see how much cash is in the bank and analyze the income statement to determine how much you typically spend per month. By dividing these figures, you will know how many months of cash you have on hand to pay bills.

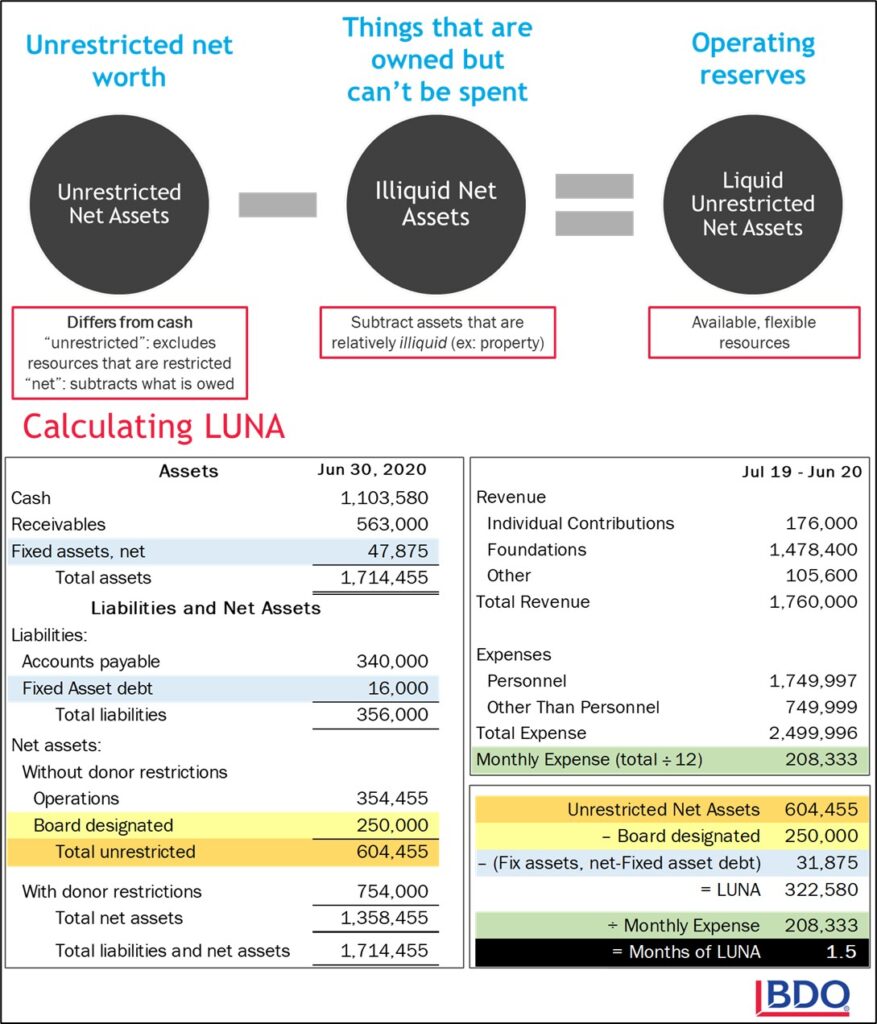

- Liquid unrestricted net assets (LUNA): Examine the balance sheet to determine the resources you have immediately available in case of emergency or to cover a cash flow issue. Here’s a tool to help you calculate LUNA.

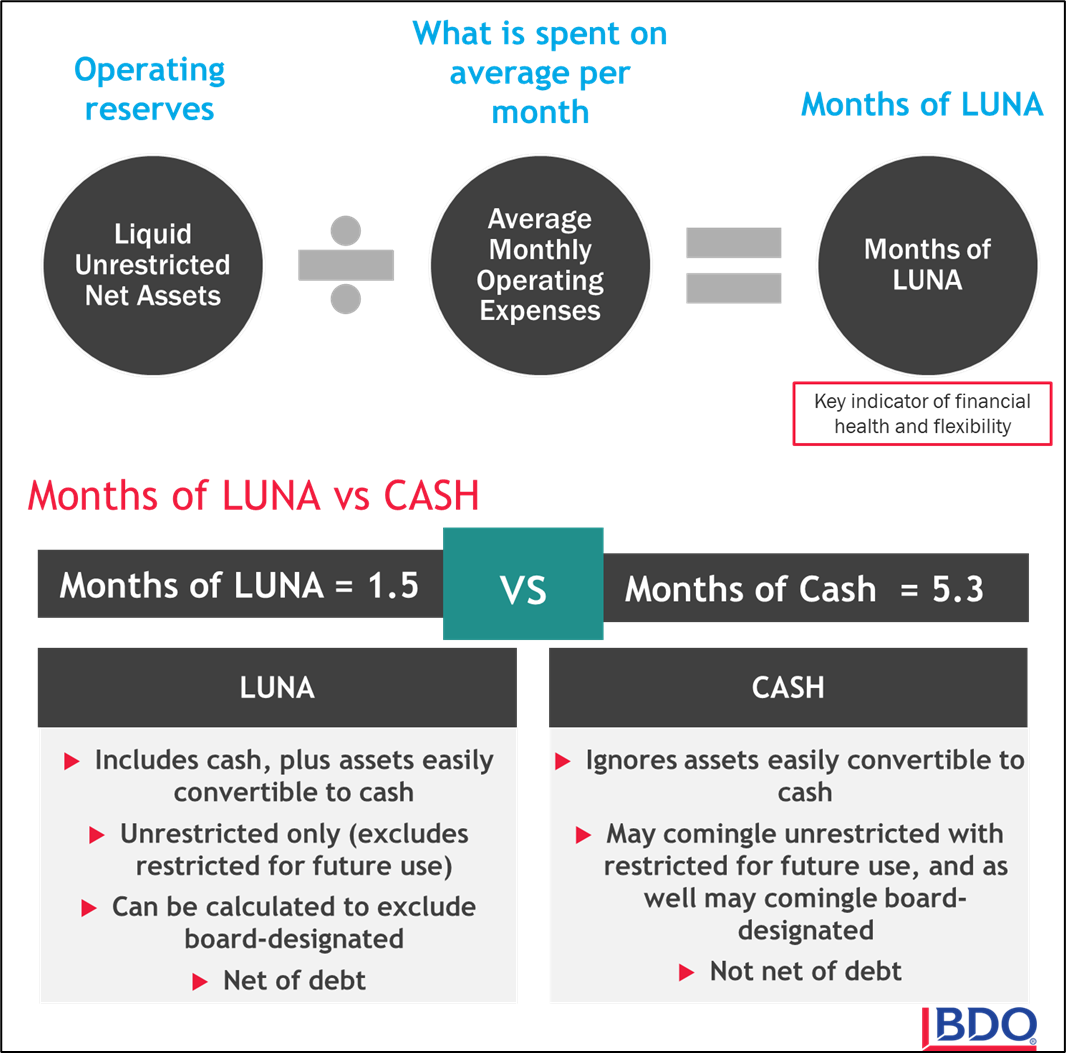

- Liquidity (months of LUNA): Similar to months of cash on hand but focused on how much liquid, unrestricted net assets you have available to cover bills. After calculating LUNA (detailed above), divide by your average monthly expense to find out how many months of LUNA you have on hand. This figure may be larger than, the same as, or less than months of cash on hand, and you may want to track both indicators or at least the more conservative one.

- Here is more detail on how to calculate these indicators and a tool for tracking these and other useful financial measures.

- Year over Year Growth

- Net Working Capital (NWC)

Find an auditor and work with them to have key reports submitted to the IRS

- Understand your state law requirements for nonprofit audits.

- Review this guide on selecting an auditor, including how to prepare for the process, solicit proposals, and interview and evaluate applicant firms.

- The main financial reports for a nonprofit organization are the income statement, balance sheet, statement of cash flows and statement of functional expenses. Based on the auditor’s recommendations, incorporate changes to better govern your finances.