Introduction

Employees’ financial wellness is directly tied to productivity, attendance, and performance, yet few employers provide comprehensive financial wellness programs. A 2014 report by the Consumer Financial Protection Bureau drew a link between financial wellness and different work outcomes, finding that 70% of American workers say financial wellness is a cause of stress, causing them to be distracted at work and negatively affecting performance. One in five employees end up missing work due to financial crises and about 61% of human resource professionals report that financial stress is impacting employee performance. Despite all of these things, only 6% of employees strongly agree that their organization assist or helps them in managing their finances, either through an employee assistance program, a HR benefit, or other activities.

Social enterprises can integrate financial wellness programming, both as a business and as a workforce program, to further increase the financial capabilities of the people they employ. But for the focus populations that many social enterprises serve, financial security is an even greater challenge. By and large, these are people back into the workforce after a long absence, moving from no-income to low-income. Many will be dependent on some, or multiple, public benefits including the Temporary Assistance for Needy Families (TANF) and the Supplemental Nutrition Assistance Program (SNAP).

While public benefits act as a safety net through the transition from unemployment back into the workforce, many of these programs have different eligibility benefits and different cut off points. As a result, managing benefits for individual budget planning can be difficult and there are still significant gaps that can occur. First, there is the coverage gap in which a person may be eligible for public benefits, but isn’t accessing them due to a lack of funding, a lack of access, or the stigma associated with receiving those benefits. There’s also what’s known as the hardship gap in which a person is receiving benefits, but still falls under the basic standard of living and financial hardship still exists. Finally, there’s the eligibility gap in which a person has earned too much money to qualify for benefits, yet does not make enough income to be self-sufficient.

Benefits Cliff

The eligibility gap, in particular, can negatively effect people employed by social enterprises. As individuals make more income while employed at a social enterprise they risk losing their benefits. For many, the gains in income increased income don’t exceed the losses in benefits that they’re incurring. This is what is known as the benefits cliff, defined as the “abrupt loss of benefits due to an increase income that affects eligibility” – the key word being “abrupt”.

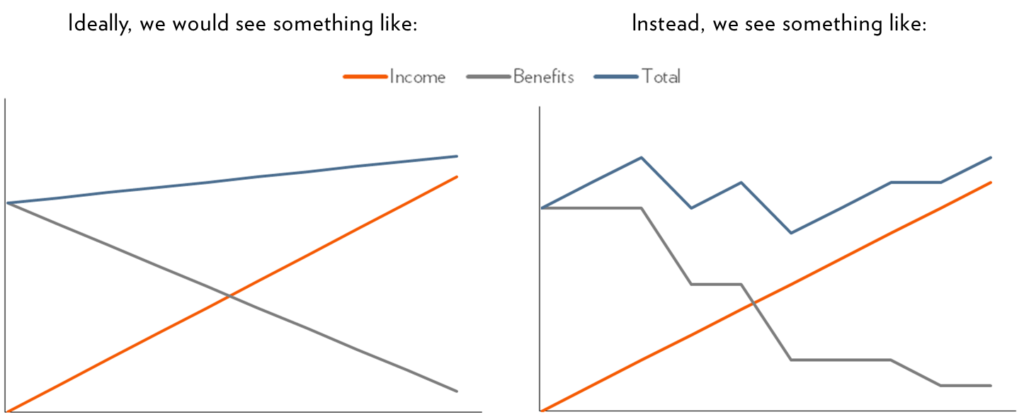

What we would like to see is that, as a person’s income increases, benefits taper off in such a way that each incremental dollar earned makes the person better off. This shouldn’t be a revolutionary concept – it is simply rewarding people for their labor. The diagram on the left below is an illustrated version of what this relationship would look like:

However, while would like this to happen, this is unfortunately not what we actually do see. Instead, we see something much closer to the diagram on the right where each incremental dollar earned doesn’t necessarily make the person better off. As they earn more money, the abrupt loss of benefits means that at certain increments they are actually worse off than they were when making less money. This breaks down a fundamental principal of rewarding people for their labor.

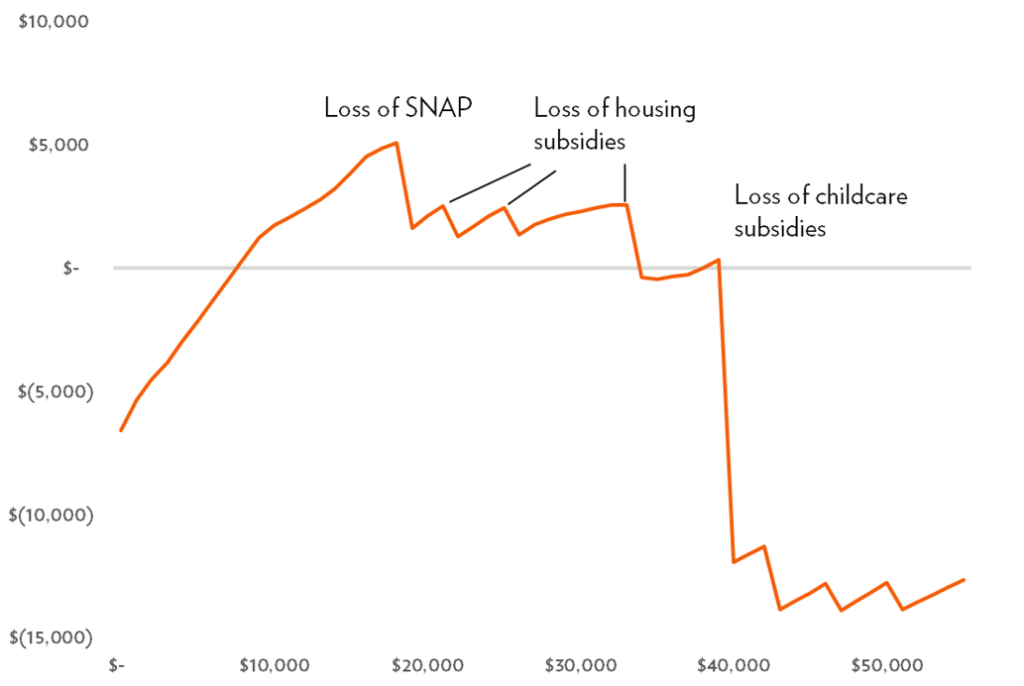

Social enterprises need to be mindful of the benefits cliff and the effects may be having on their employees. We must be mindful that the typical we think about income and income increases doesn’t necessarily apply. A useful tool in helping you understand the effects of the benefits cliff, is the Family Resource Simulator created by the National Center for Children in Poverty. It allows you to graph the impact of public benefits on different focus populations in different geographies. Below is an example for a single adult, with one dependent, living in San Francisco:

At first, we see the linear relationship that we’d like to see: an increase in earned income makes the person better off. However, at around $20,000 in income that relationship begins to break down. There are now abrupt moments when the increase in income triggers a loss of a benefit, ultimately making the person worse off with incremental earned income. This becomes particularly pronounced at the higher end with $40,000 or more, when childcare subsidies are jeopardized. As you can see, while we refer to the benefits cliff, what we really are dealing with is benefit’s cliffs.

Of course, this will vary considerably from person to person, in geography to geography, so it shouldn’t replace understanding an individual’s path as best you can. However, this is still a useful exercise for a social enterprise to do for representative members of their focus population, in order to be mindful of the types of experiences their employees may be going through as they transition back into the workforce.

Employee Supports

While there are policy fixes in place to curb the effects of the benefits cliff, social enterprises must deal with the world as it exists, not as it should be. So what can social enterprises do to assist their employees? Comprehensive employee support programs are part of what set social enterprises apart from traditional employers. Financial literacy alone is not going to be enough to build a person’s financial capabilities. Instead, a person will need financial literacy combined with increased access to actual financial products and services. There are a number of ways that financial wellness can be incorporated into a social enterprise’s employee support program. Offerings such as:

- Benefits screening

- Income and benefit planning

- Facilitating bank accounts and direct deposit

- Funds for barrier removal or employment related expenses

- Tax preparation

- Retention bonuses

- Matching savings and earning supplements

A financial wellness program can be implemented at transitional social enterprises, workforce agencies, and permanent employers. A successful program will be focused both on addressing and preventing crises, and assisting individuals with their long term goals. Financial wellness programs should include educational programming on topics such as budgeting and money management, debt reduction, credit score management and financial goal setting. These educational resources should be offered in combination with programs that increase access to financial products in order to boost overall financial inclusion and capability.

In order to structure a financial wellness program, first find the metrics you want to measure for the population you work with. Metrics that can help evaluate an individual’s financial health include that person’s:

- Assets

- Credit score

- Debt burden

- Level of emergency savings

- Access to a bank account

From the very beginning of your program, or of an employee’s tenure at your business, talk about financial wellness and introduce both the programming you offer and the financial products you provide access to. Include peer-to-peer strategies and opportunities for employees to talk to each other and build a safe space, creating a supportive and collaborative work environment.

Educational programming can be implemented in three different ways:

- One-to-one counseling

- One-to-one coaching

- Group workshops

The difference between counseling and coaching is that counseling sessions are focused on more immediate remediation and crisis solving, whereas coaching is a series of touch points to break long-term financial goals into intermediate milestones. For all of the above, it is a best practice to introduce these offerings at orientation.

The Broader Strategy

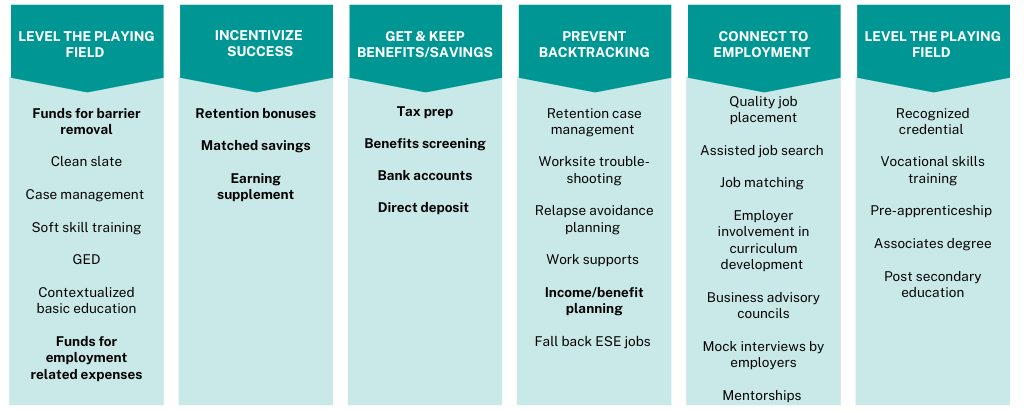

As stated, it’s important not to address financial literacy in isolation, but instead do it in combination with employee supports that improve financial inclusion through increased access to financial products. Similarly, it is important not to address financial capability in isolation, but instead do it as part of a broader employee supports strategy. The diagram below illustrates how financial capability employee supports can support the broader goals of an employee supports program:

The supports highlighted in the above diagram are related to financial well-being in some way. You can see how essential these supports are in achieving the broader goals, especially incentivizing success and keeping benefits and earnings. As a result, it’s important that we think about these employee supports working together in concert, delivering not just financial well-being for employees, but holistic well-being of which finances are a part.