Introduction

Before your social enterprise can evaluate different pricing strategies for its products, it must first understand two crucial pieces of information. The first is the costs associated with making its products or delivering its services, known as the “cost structure” of a business. The second is the price or the volume that it would require to break-even.

In this deep dive, we will learn how to:

- Understand your social enterprise’s cost structure

- Conduct a break-even analysis

1. Understanding your cost structure

A business’ cost structure is the combination and relative proportions of all of the costs associated with running its business and producing products for the market. Understanding the cost structure is essential in order to inform how a business prices its goods or services, as well as allowing a business to identify potential areas for cost reduction. To start, you must understand the difference between fixed and variable costs.

Fixed and variable costs

Every type of cost your social enterprise incurs can be categorized as either a “fixed” or a “variable” cost.

Fixed costs are those costs that your business incurs regardless of production. These include:

- Salaries paid to employees

- Rent

- Employee supports

Variable costs are those costs that change relative to the amount produced. These include:

- Materials used in making the product

- Selling expenses

- Billable staff wages

Example

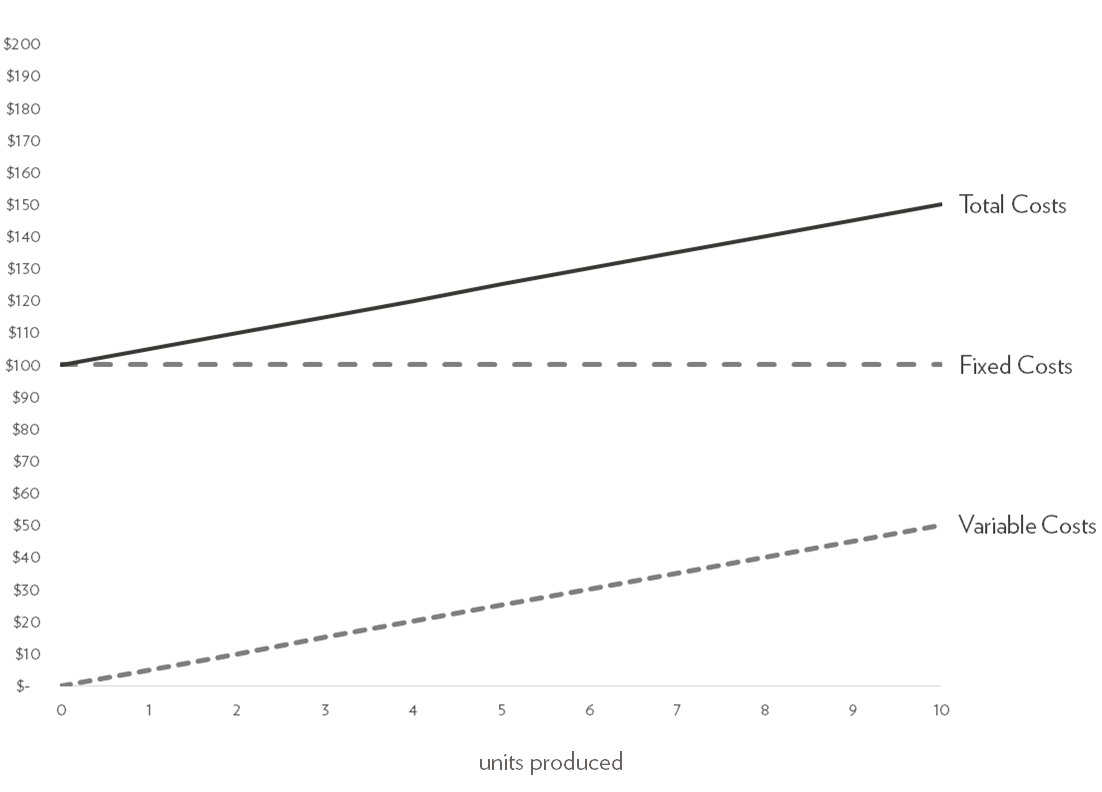

Let’s say a social enterprise has $100 in fixed costs per month and variable costs of $5 per unit. This means that even if they produce 0 units, the enterprise incurs $100 in costs every month. With each incremental unit produced per month, the enterprise incurs $5 in additional costs. If they produce 1 unit per month, they incur the $100 in fixed costs plus the $5 in variable costs, for a total of $105 in costs. If they produce 2 units, they incur the $100 in fixed costs plus a total of $10 in variable costs. And so on. Represented graphically, it would look like this:

This is not normally something you need to graph (and $100 in fixed costs is unrealistically low), but in this case it helps us visually understand how costs increase with each incremental unit produced. It also sets up our next step: the break-even analysis.

2. Conducting a break-even analysis

Once a social enterprise properly understands its costs, the next step is to conduct a break-even analysis. A break-even analysis is a simple bit of arithmetic that tells you:

- How much quantity you’d have to sell at a given price in order to break-even or

- What you need to charge for a fixed quantity of goods in order to break-even

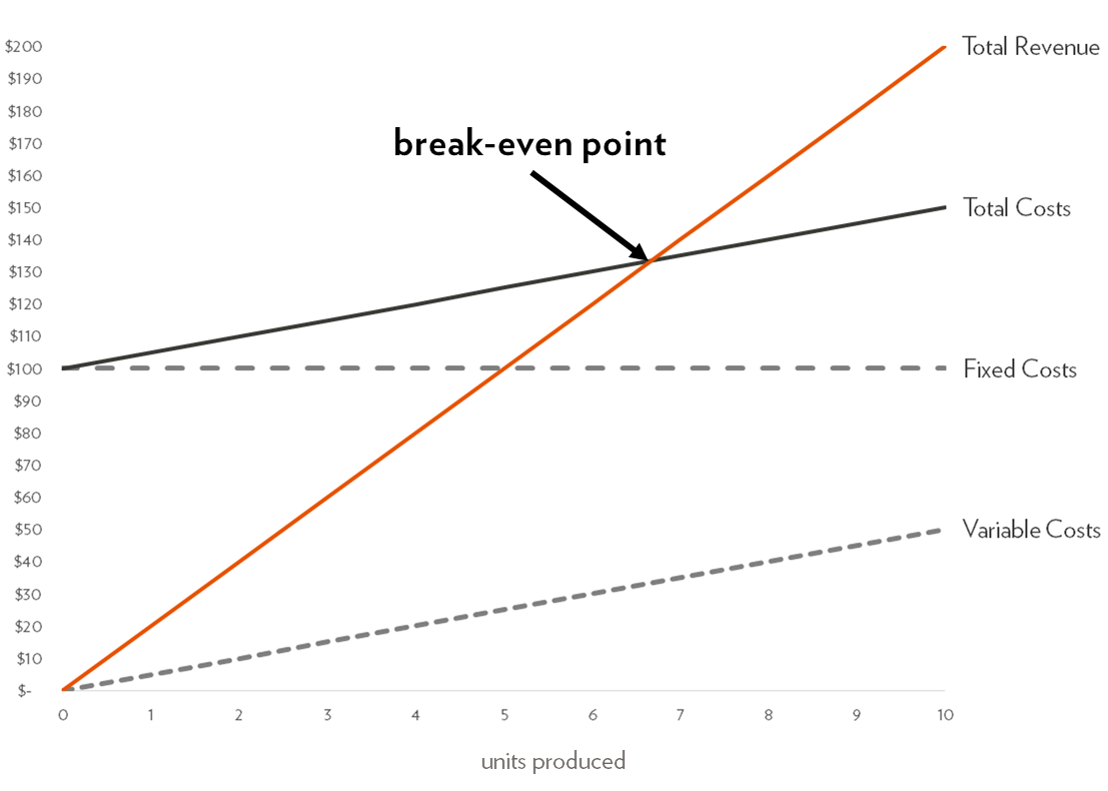

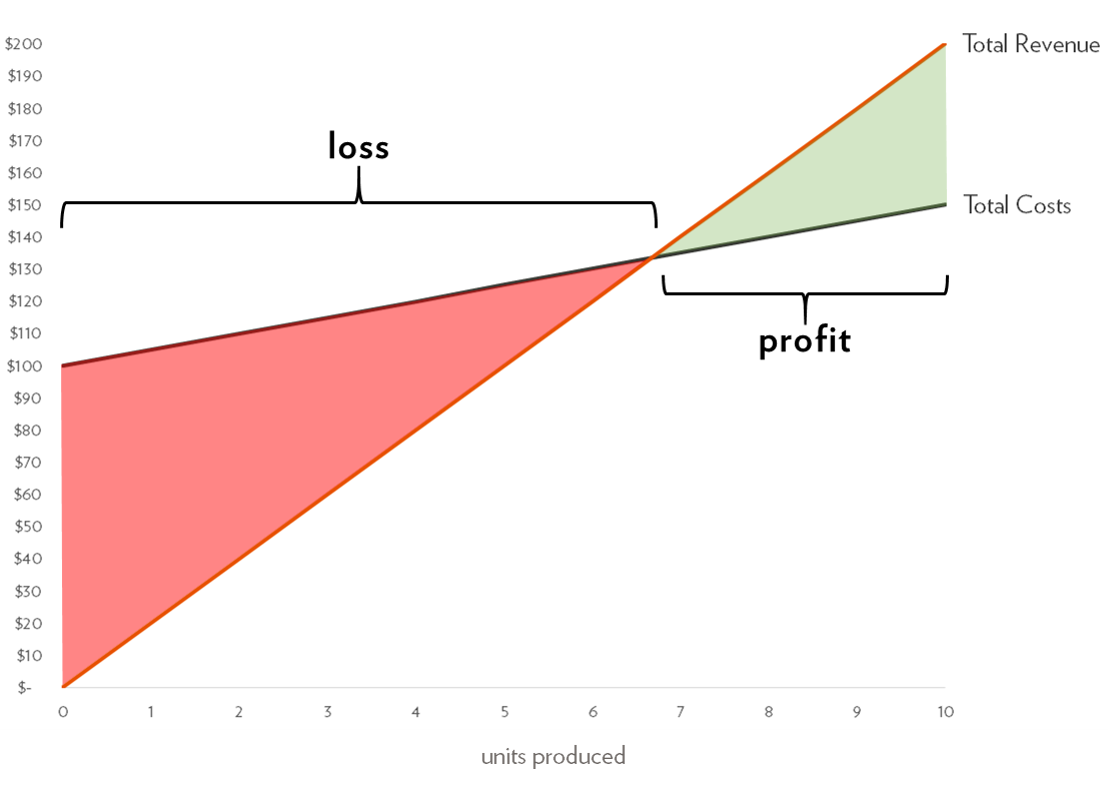

Using the social enterprise example above, if they set their prices at $20 per unit we can graph how their revenue increases with each unit sold and see the point at which they would break-even:

In this example, the social enterprise must sell 7 or more units in order to cover the fixed and variable costs associated with producing the 7 units. Selling 6 or fewer units will result in an overall loss for the social enterprise. Selling 7 or more units will result in a profit, one that increases with each incremental unit sold.

Calculate break-even price or volume

Now let’s try with your own numbers. In the equation below, put in your social enterprise’s fixed and variable costs and the target selling price per unit in order to determine the quantity you would need to sell in order to break-even.

fixed costs / (price – variable costs) = break-even volume

This type of calculation can also be done if you have a fixed amount you’re able to produce in a given amount of time. In the above example, let’s assume the social enterprise can produce no more than 100 units per month. Assuming maximum production per month, and that all units produced are sold, what price would they need to charge in order to break-even each month? You can calculate with the below equation:

(fixed costs / volume) + variable costs = break-even price

What do we really mean by “break-even”?

Depending on the organizational structure of your social enterprise, the meaning of “break-even” might not be so straightforward. Accounting for social costs (costs incurred by your social enterprise above and beyond ordinary business costs in order to fulfill its mission) adds an additional layer of complication as well. This is particularly true for those social enterprises that are a subsidiary of a parent non-profit organization. For these social enterprises, breaking-even could be thought of more broadly from an agency perspective, or more narrowly from just a social enterprise perspective.

For example, an organization may have a full-time case manager on staff to work with the social enterprise employees. Depending on how the organization and social enterprise’s accounting is done, this position may be included on the organization’s profit and loss statement (P&L) and not the social enterprise’s. If this organization is thinking about breaking-even from an agency perspective, these costs should be included in our calculation. On the other hand, if they are thinking only about breaking-even from a social enterprise perspective, they need only include those costs on the social enterprise’s P&L.

Alternatively, an organization or social enterprise may simply want to understand the point at which business revenues cover business costs. In this case, they might exclude social costs altogether, though they should be aware that the break-even point they calculate won’t necessarily lead the social enterprise to be fully sustainable.

Ultimately, it is up to your social enterprise to determine what it means to “break-even”. Use the calculators above to test different scenarios, including and excluding social costs or agency costs, if appropriate.

Conclusion

However you determine what it means to break-even for your social enterprise, from a pricing perspective the goal often is to do better than merely break-even on each unit sold. That’s why understanding your social enterprise’s costs and break-even price (or volume) is just the first step in a successful pricing strategy. We’ve developed a template for you to use, to try out what you’ve learned here!